The Brazilian Energy Distribution System

Last updated: 27 January 2016

The Brazilian energy distribution system represents a critical aspect of the country’s infrastructure. In this article we will present an overview of Brazil’s energy distribution system.

Main Regulators and Government Agencies

The current energy distribution system in Brazil was planned and developed during the middle of the 1990’s, and only updated during 2004. Similarly to the sector of telecommunications, the national energy system underwent a restructuring process during the end of the 20th century with the goals of establishing a regulated yet efficient structure for energy generation, transmission and distribution.

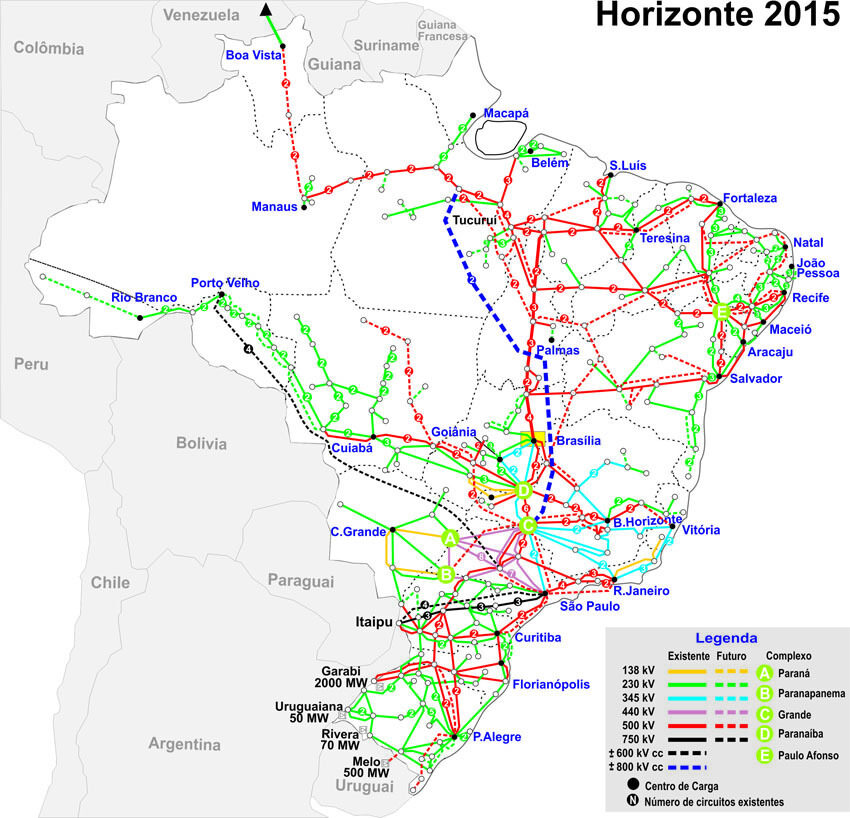

One of the main results of this reform was the establishment of the Sistema Interligado Nacional, or NIS, Portuguese for National Interconnected System, which is the name of the interlinked power grid that serves all Brazilian states and emcompasses over 98% of all the energy produced in the country. Although the regulatory changes allowed for the private sector to take part in multiple aspects of the SIN, such as taking part in concession contracts to operate in multiple parts of the system, the new model still retained a number of crucial roles for government agencies, most of which are associated with the Brazilian Ministry of Mines and Energy.

Some of the main entities in charge of regulating and operating the national energy system include the:

- National Electrical System Operator, or ONS: Organisation responsible for operating and coordinating the energy generation and transmission systems of SIN

- Brazilian Electricity Regulatory Agency, or ANEEL: Government agency responsible for regulating the national energy matrix and related markets

- Chamber of Commercialisation of Electrical Energy, or CCEE: Main operator of the electricity market in Brazil, responsible for monitoring the prices for energy distribution, advising on the activities of national power plants and for launching auctions for generation and distribution contracts

In general terms, the energy sector in Brazil can be considered highly centralised and firmly regulated by the state. Some examples of the state control include the requirement for private players to take part in auctions and concession agreements to enter the national market and also price-fixing for the segments of transmission and distribution.

Power Grid Overview

The SIN grid is divided into multiple interconnected distribution complexes that transport electricity to various regions of the country. The grids structure allows for power plants in various regions to feed into the same central lines, a factor that contributes to increasing the overall resilience of the national energy system.

The main energy transportation complexes are composed of high-voltage transmission lines. According to national regulation, power lines that operate at over 230 KV are categorised as transmission lines, while those that operate at an inferior voltage are categorised as distribution lines. These are those that are closer to reaching the end users and in Brazil are usually set at voltages of 13.8 KV or 34.5 KV. ANEEL’s data indicate that there are currently over 125.000 km of installed transmission lines.

Energy Sources

One of the main motivators for the establishment of a centralised structure of operations of the Brazilian energy distribution system was to prevent any region of the country to be subject to deficits in power distribution in case of failures of extended climate disorders. Most of the risks for supply crisis are related to its most important types of power plants, which are hydroelectric plants.

This category of energy generators is occasionally at risk of suffering from droughts and other weather-related issues, which might compromise their capacity to feed into the national power grid. In the cases where hydroelectric plants are unable to supply sufficient energy to the SIN, other types of power plants such as thermoelectric are activated in order to cope with the national demand at the consequence of raising the price of energy to end users. According to data from 2015 by ANEEL, the most important types of power plants in Brazil in terms of the total energy generated in the country are:

- Hydroelectric

- Thermoelectric

- Eolic

- Thermonuclear

- Other

The total energy generation capacity in Brazil currently sits above 135 GW. Many of the largest hydroelectric power plants in the country, such as the Itaipu and Tucurui plants, each contribute over 7 GW to the national energy system, making them crucial parts of the country’s power grid. Thermoelectric plants can be found in larger numbers, although their generation capacity are in most cases inferior to hydroelectric plants. A notable example is the thermoelectric complex of the city of Capivari de Baixo, in the state of Santa Catarina, which is the largest in South America and presents total capacity of energy generation of 853 MW.

Brazil also holds 2 thermonuclear plants, located in the same complex in the city of Angra dos Reis, which combined generates close to 2 GW. In the last few years, Brazil has invested significantly in the creation of new power plants that make use of renewable energy resources, such as eolic and solar plants, which currently make up for over 4% of the total national energy capacity.

National Market

The restructuring of the energy sector in Brazil has allowed for national public companies to receive significant private investments, although most of the control over the main companies, particularly in the segment of energy generation, remain controlled by the country’s state. For example, the largest player in this market, the state-controlled and publicly traded company Eletrobrás, represents a holding of some of the main energy generation companies in Brazil, and in total encompasses over 37% of the power generation capacity and holds 57% of the power distribution lines in the country.

According to data from ANEEL, as of 2015 Brazil held close to 1,000 players in the national market, operating in segments of generation, transmission, distribution and commercialisation of energy, with the vast majority being categorised as independent producers. Segments such as distribution are divided into a small number of companies, or over 45, due to the concession model adopted in the country where each one of these players is assigned a monopole over a determinate region.

Currently the most relevant energy distribution companies operating in Brazil, in terms of distributed power, include:

- Eletropaulo (Serves the metropolitan region of the city of São Paulo): 10.4%

- Cemig (Serves the state of Minas Gerais): 7.5%

- Copel (Serves the state of Paraná): 7.0%

- Light (Serves the state of Rio de Janeiro): 7.0%

- CPFL Energia (Serves the state of São Paulo): 6.6%